Executive Summary

The present report has three parts. In part 1, there was need to determine whether ANZ should report the ASIC allegation on BBSW manipulation, and if yes, how it should be treated in their 2016 annual financial statement. It was established that the entity was required to report the same in order to have their financial statements present a true and fair financial position, performance and cash flows in line with AASB 101.15. This was to be included as a note to the financial statements, given that it was a contingent liability, in line with AASB 137.86, AASB 101.13 and numerous provisions of the Corporations Act of 2001. In part 11 (a), it was determined that the fine payment imposed on ANZ was to be recorded and reported as a liability having satisfied the criteria in CF.49, 60 and 64, as well as AASB 137.37 and AASB 137.13 (a). Elsewhere, the “Assured Overdraft investigation” was to be treated as a contingent liability in the 2015 annual financial statements in line with AASB 137.13 (b) and recorded in the director’s notes as per AASB 137.86 . Given that the fine was certain in amount by 2016, it would be treated as a provision and recorded as a liability as given by AASB 137.13 (a). The last section had four questions. In part (a), it was apparent that business and other commercial loans should be treated as assets, current or non-current depending on whether they could be realized within a year after the reporting period. This was supported by The CF. 53, CF 55 (a) – (d) and AASB 101.66. In the second part (b) of the question, debt-to-equity-ratio and central bank policy were identified as the main factors affecting the value of financial assets in ANZ. Part (c) explained that the appropriate way to write off bad debts was to include them as an expense in the income statement while making adjustments in accounts receivables as supported by CF.94. Finally, the impact of loan defaulting on ANZ’s financial position would be a reduction in assets and equity (CF.53.). Elsewhere, the effect on financial performance would be increased expenses and reduced income as given in CF.74.

Part 1: Investigation by ASIC

The ASIC investigation into ANZ bank needed to be reported in their 2016 financial statements. Under fair representation and compliance with IFRS, AASB 101.15 requires entities to fairly present their financial position, performance and cash flows including other items. More importantly, they are required to make additional disclosures when deemed necessary in order to attain the fairness standard. In this respect, ANZ needed to disclose the investigation in addition to its compliance to IFRS in order to give a fair and true view of their financial statements. Though additional disclosure is only given on a necessity basis, the fact that the investigation had a possible impact on the bank’s financial performance in the near future sufficed. AASB 101.17(c) adds that; to achieve the fair standard an entity must make additional disclosure when the mere compliance to the Australian Accounting Standards do not provide enough information for the understanding of various transactions and their impact and other essential events in the financial statements. This puts it beyond doubt that the ASIC investigation needed to be reflected in ANZ’s 2016 financial statements. However, as a contingent liability, the investigation is only to be disclosed in line with AASB 137.86 that requires the nature of the obligation expected, its effects and any uncertainties as per the economic outflows to follow.

The investigation on the Bank Bill Swap Rate (BBSR) breach should be reported under the director’s notes. Under the Corporations Act of 2001 S.295.1, an annual financial report encompasses the financial statements for the year, the notes accompanying the financial statements and the director’s declaration regarding the financial statements and notes. In the description of the notes to the financial statements, ss.295.3 of the Act and S.297 requires that the notes provide additional disclosures that are necessary for the financial statements to reflect a true and fair view of the organization’s financial position. AASB 101.10 (e) also states that a complete set of financial statements shall include notes on other explanatory information which in this case entails the investigation in question. Thereby, it is in the notes that the director would reveal the ongoing investigation in order to meet the fair standard. AASB 101.13 also states that a management review should accompany the financial statements in order to explain the factors affecting financial performance and what steps the entity has taken in response to such influences.

Part 11: ASIC Fine

2 (a) The recording and reporting of the fine payment should be under the classification of liabilities. According to the Conceptual Framework (CF).49, a liability is a present obligation arising from past events or transactions whence the settlement encompasses an outflow of resources that are tantamount to economic benefit. This broad definition affirms that the fine payment should be recorded as a liability, given that the sum was as a result of a past event (ASIC investigation and ANZ assured) and the company would lose economically ($212,500 settlement). The CF.60 also describes a present obligation as an essential facet of a liability, implying that a party is required to act in a certain way that is legally enforceable. This condition is also met, with ANZ obligated to pay the fine to ASIC or face precipitate action. Though the liability involves uncertainty in timing, the CF.64 takes care of such a conflict. It recognizes that in some instances, liabilities involving any form of estimation in amount or timing are treated as provisions by entities, but as long as they constitute a present obligation and other requirements in CF.49, it should be treated as a liability. This was the case in the fine payment, and in essence, the amount to be paid was not up for approximation. This effectively means that the fine payment needed to be recorded as a liability. AASB 137.13 (a) reaffirms this by the express statement that provisions are recognized as liabilities due to having a present obligation and leading to an outflow of resources that would have otherwise constituted an economic benefit. Therefore, whether the fine was to be looked at from the general definition of a liability or as a provision, it still fitted to be recorded as a liability. It should be noted that in the case above, uncertainty in the amount to be paid as settlement would have not changed the liability status of the fine payment. This is because AASB 137.37 provides clear guidelines for the determination of the best estimate needed to settle the present obligation within the reporting period.

2 (b) Reporting of ANZ Assured Investigation

The reporting of the ANZ Assured overdraft investigation by ASIC should be reflected in the director’s notes as a contingent liability in the 2015 annual financial report but as a provision in the 2016 financial report. The reason for presenting as notes for the 2015 financial year has been highlighted in AASB 137.13 (b) which states that such should not be listed as liabilities because it is yet to be known if such events suffice a present obligation that would lead to an outflow of economic resources. ANZ could only provide disclosure notes in this respect given that they were unsure on the outcome of the investigation. Additionally, if there was a present obligation that was not clear on the estimate of the amount of obligation that shall be required or if there would be an outflow of economic resources, still the investigation would have been treated as a contingent liability rather than a recognizable liability. The decision to present a contingent liability in form of notes is clearly demonstrated in AASB 137.86 where details about the nature of the contingent liability, its possible financial effects, possibility of reimbursement and the uncertainties regarding timing or amount of outflow are required. However, for the 2016 financial report, the investigation would be recognized as a provision and hence recorded as a liability. This is because the fine amount was already known and there was a present obligation posed to the company. Recognizing the investigation as a provision and subsequent recording of it as a liability is supported by AASB 137.13 (a) citing present obligation and certainty of economic outflow of resources.

Part 111: Bad Debts

3 (a) Business and other commercial loans should be reported as assets in the 2016 financial year. Unlike other businesses, loans are assets to the banks because they generate their profits from charging interest on such. The CF. 53 highlights future economic benefits as the key characteristic of an asset, whereas such benefits contribute directly or indirectly to the flow of cash/cash equivalents in the company. In this case, loans contribute to the flow of cash in form of interest which qualifies them as an asset. CF. 55 (a) – (d) explains the various examples of how the economic benefits of assets can flow. These include being used to settle another liability, exchanged for other assets, usage to produce goods and services and so forth. In that respect, loans have ability to generate interest that can settle liabilities or even be used in the production of other goods and services. They also have exchange value given that customers often offer security in return for loans. Elsewhere, there is a misconception oftentimes made that assets must be tangible, but the above section further deconstructs such a narrative explaining that intangibility does not disqualify asset status. More specifically, loans should be treated as non-current assets. This is because they are long term in nature and are further likely to be defaulted on. AASB 101.66 is clear that any asset that cannot be realized within a period of 12 months after the reporting period should be classified as non-current. However, if there are short term loans whose realization was within 12 months after the reporting period and further were at no risk of default, such would qualify as current assets. This was however unlikely given the company’s anticipated $100m bad debt blowout.

3 (b) One of the banking sector related factors likely to impact on the value of financial assets at ANZ was the debt-to-equity ratio. Currently, the ratio was high implying that the company was engaging in risky investments and in particular, there was more debt than equity funding its assets. The effect of such a scenario is twofold. If there was high interest cost and no substantial increase in net profits, then shareholders would end up at a loss (Athanasoglou, Brissimis and Delis 2008). Elsewhere, if the net profit superseded the interest cost then the shareholders would realize profits from the scenario. The debt to equity ratio being high should not be necessarily a cause for alarm, as there may be high profits in the end which shall improve the value of financial assets. However, it can also lead to devaluation of financial assets given that the bank was engaging in high risk investments. Another factor is the central bank policy, which governs interest rates and issues other guidelines with respect to both short term and long term loans. If there are favorable regulations for instance high interest rates, removal of interest rate caps and so forth, the bank will experience a boom in their financial services (Athanasoglou, Brissimis and Delis 2008). In the same way, unfavorable policy like low interest rates may increase borrowing and reduce profitability at the same time.

3 (c) The best method of writing off bad debts from the company’s 2016 annual financial statements is to recognize them as an expense in the income statement and reflect an adjustment in the accounts receivables. According to CF.94, an expense is treated in such a manner when there is a decrease in the expected future benefits with respect to an asset or an increment in liability that can be measured accurately. In this case, it is apparent that bad debts were a reduction in assets and therefore qualified for recognition as expenses. The company was also in a position to reliably estimate the amount to be written off. As mentioned before, loans are assets to a bank and therefore the reduction presented in the case scenario suffices a bad debt expense. The inclusion on the income statement should be made immediately the assets (loans) fail to qualify as assets in the balance sheet. This implies that the company would need to make adjustments in pg.62 of the annual financial report and accordingly introduce the expense. In the same way, there would be an adjustment on pg.63 which presents the balance sheet, particularly a reduction on accounts receivables.

3 (d) The financial position of an organization is defined by assets, liabilities and equity. Defaulting of the loans will lead to reduction of assets and equity in the organization. Assets are defined under The CF. 53 and basically constitute future economic benefits. The assets in question in this case are loans and they will thus definitely reduce following their writing off and conversion into expenses in the income statement. Equity will reduce as a result of reduction in assets even if liabilities do not increase. This is because equity is determined by the amount of assets less liabilities. In terms of financial performance, there shall be reduced income and increased expenses. Income shall reduce due to loss of the revenue and gains described in CF.74 such as the inability to sale non-current assets. Most of the defaulted loans fall under the latter category and thereby lead to reduction in income. Elsewhere, expenses shall increase in the sense that bad debts are often recorded as expenses in the income statement. CF.78 defines expenses as those economic losses arising in the course of the ordinary activities of the organization or in separate scenarios. Defaulting of loans in this case is a loss emanating from normal activities of the entity and thus constitutes an increase in expenses.

References

Athanasoglou, P.P., Brissimis, S.N. and Delis, M.D., 2008. Bank-specific, industry-specific and macroeconomic determinants of bank profitability. Journal of international financial Markets, Institutions and Money, 18(2), pp.121-136.

Australian Accounting Standards Board, 2011. ASB 101: Presentation of Financial Statements. Commonwealth of Australia. Retrieved from http://www.aasb.gov.au/admin/file/content105/c9/AASB101_09-07_COMPmay11_07-11.pdf

Australian Accounting Standards Board, 2014. ASB 137: Provisions, Contingent Liabilities and Contingent Assets. Commonwealth of Australia. Retrieved from http://www.aasb.gov.au/admin/file/content105/c9/AASB137_07-04_COMPjun14_04-14.pdf

Australian Accounting Standards Board, 2016. Compiled Framework: Framework for the Preparation and Presentation of Financial Statements. Commonwealth of Australia. Retrieved from http://www.aasb.gov.au/admin/file/content105/c9/Framework_07-04_COMPjun14_07-14.pdf

Australian and New Zealand Bank, 2016. Annual Report. Australia and New Zealand Banking Group. Retrieved from http://www.shareholder.anz.com/sites/default/files/anz_-_annual_report_2016.pdf

Federal Register of Legislation n.d. Corporations Act 2001. Retrieved from https://www.legislation.gov.au/Details/C2013C00003

Appendices

AASB 101.15

Fair Presentation and Compliance with IFRSs 15

Financial statements shall present fairly the financial position, financial performance and cash flows of an entity. Fair presentation requires the faithful representation of the effects of transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Framework. The application of IFRSs, with additional disclosure when necessary, is presumed to result in financial statements that achieve a fair presentation.

AASB 101.17(c)

to provide additional disclosures when compliance with the specific requirements in Australian Accounting Standards is insufficient to enable users to understand the impact of particular transactions, other events and conditions on the entity’s financial position and financial performance.

AASB 137.86

Unless the possibility of any outflow in settlement is remote, an entity shall disclose for each class of contingent liability at the end of the reporting period a brief description of the nature of the contingent liability and, where practicable: (a) an estimate of its financial effect, measured under paragraphs 36-52; (b) an indication of the uncertainties relating to the amount or timing of any outflow; and

(c) the possibility of any reimbursement.

AASB 137.13 (a)

provisions – which are recognised as liabilities (assuming that a reliable estimate can be made) because they are present obligations and it is probable that an outflow of resources embodying economic benefits will be required to settle the obligations; and

AASB 137.37

The best estimate of the expenditure required to settle the present obligation is the amount that an entity would rationally pay to settle the obligation at the end of the reporting period or to transfer it to a third party at that time. It will often be impossible or prohibitively expensive to settle or transfer an obligation at the end of the reporting period. However, the estimate of the amount that an entity would rationally pay to settle or transfer the obligation gives the best estimate of the expenditure required to settle the present obligation at the end of the reporting period.

AASB 137.13 (b)

contingent liabilities – which are not recognised as liabilities because they are either: (i) possible obligations, as it has yet to be confirmed whether the entity has a present obligation that could lead to an outflow of resources embodying economic benefits; or (ii) present obligations that do not meet the recognition criteria in this Standard (because either it is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation, or a sufficiently reliable estimate of the amount of the obligation cannot be made).

AASB 101.66

An entity shall classify an asset as current when: (a) it expects to realise the asset, or intends to sell or consume it, in its normal operating cycle; (b) it holds the asset primarily for the purpose of trading; (c) it expects to realise the asset within twelve months after the reporting period; or (d) the asset is cash or a cash equivalent (as defined in AASB 107) unless the asset is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period. An entity shall classify all other assets as non-current.

AASB 101.13

Many entities present, outside the financial statements, a financial review by management that describes and explains the main features of the entity’s financial performance and financial position, and the principal uncertainties it faces. Such a report may include a review of: (a) the main factors and influences determining financial performance, including changes in the environment in which the entity operates, the entity’s response to those changes and their effect, and the entity’s policy for investment to maintain and enhance financial performance, including its dividend policy; (b) the entity’s sources of funding and its targeted ratio of liabilities to equity; and (c) the entity’s resources not recognised in the statement of financial position in accordance with IFRSs.

(CF).49

The elements directly related to the measurement of financial position are assets, liabilities and equity. These are defined as follows: (a) An asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity. (b) A liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits. Equity is the residual interest in the assets of the entity after deducting all its liabilities.

(CF).60

An essential characteristic of a liability is that the entity has a present obligation. An obligation is a duty or responsibility to act or perform in a certain way. Obligations may be legally enforceable as a consequence of a binding contract or statutory requirement. This is normally the case, for example, with amounts payable for goods and services received. Obligations also arise, however, from normal business practice, custom and a desire to maintain good business relations or act in an equitable manner. If, for example, an entity decides as a matter of policy to rectify faults in its products even when these become apparent after the warranty period has expired, the amounts that are expected to be expended in respect of goods already sold are liabilities.

(CF).64

Some liabilities can be measured only by using a substantial degree of estimation. Some entities describe these liabilities as provisions. In some countries, such provisions are not regarded as liabilities because the concept of a liability is defined narrowly so as to include only amounts that can be established without the need to make estimates. The definition of a liability in paragraph 49 follows a broader approach. Thus, when a provision involves a present obligation and satisfies the rest of the definition, it is a liability even if the amount has to be estimated. Examples include provisions for payments to be made under existing warranties and provisions to cover pension obligations.

The CF. 53

The future economic benefit embodied in an asset is the potential to contribute, directly or indirectly, to the flow of cash and cash equivalents to the entity. The potential may be a productive one that is part of the operating activities of the entity. It may also take the form of convertibility into cash or cash equivalents or a capability to reduce cash outflows, such as when an alternative manufacturing process lowers the costs of production.

The CF. 55 (a) – (d)

The future economic benefits embodied in an asset may flow to the entity in a number of ways. For example, an asset may be: (a) used singly or in combination with other assets in the production of goods or services to be sold by the entity; (b) exchanged for other assets; (c) used to settle a liability; or (d) distributed to the owners of the entity.

CF.94

Expenses are recognised in the income statement when a decrease in future economic benefits related to a decrease in an asset or an increase of a liability has arisen that can be measured reliably. This means, in effect, that recognition of expenses occurs simultaneously with the recognition of an increase in liabilities or a decrease in assets (for example, the accrual of employee entitlements or the depreciation of equipment).

CF.74

The definition of income encompasses both revenue and gains. Revenue arises in the course of the ordinary activities of an entity and is referred to by a variety of different names including sales, fees, interest, dividends, royalties and rent.

Coporations Act, 2001

S. 295.1

1) The financial report for a financial year consists of:

(a) the financial statements for the year; and

(b) the notes to the financial statements; and

(c) the directors’ declaration about the statements and notes.

ss.295.3

The notes to the financial statements are:

(a) disclosures required by the regulations; and

(b) notes required by the accounting standards; and

(c) any other information necessary to give a true and fair view (see section 297)

s. 297

True and fair view

The financial statements and notes for a financial year must give a true and fair view of:

(a) the financial position and performance of the company, registered scheme or disclosing entity; and

(b) if consolidated financial statements are required–the financial position and performance of the consolidated entity.

This section does not affect the obligation under section 296 for a financial report to comply with accounting standards.

Note: If the financial statements and notes prepared in compliance with the accounting standards would not give a true and fair view, additional information must be included in the notes to the financial statements under paragraph 295(3)(c).

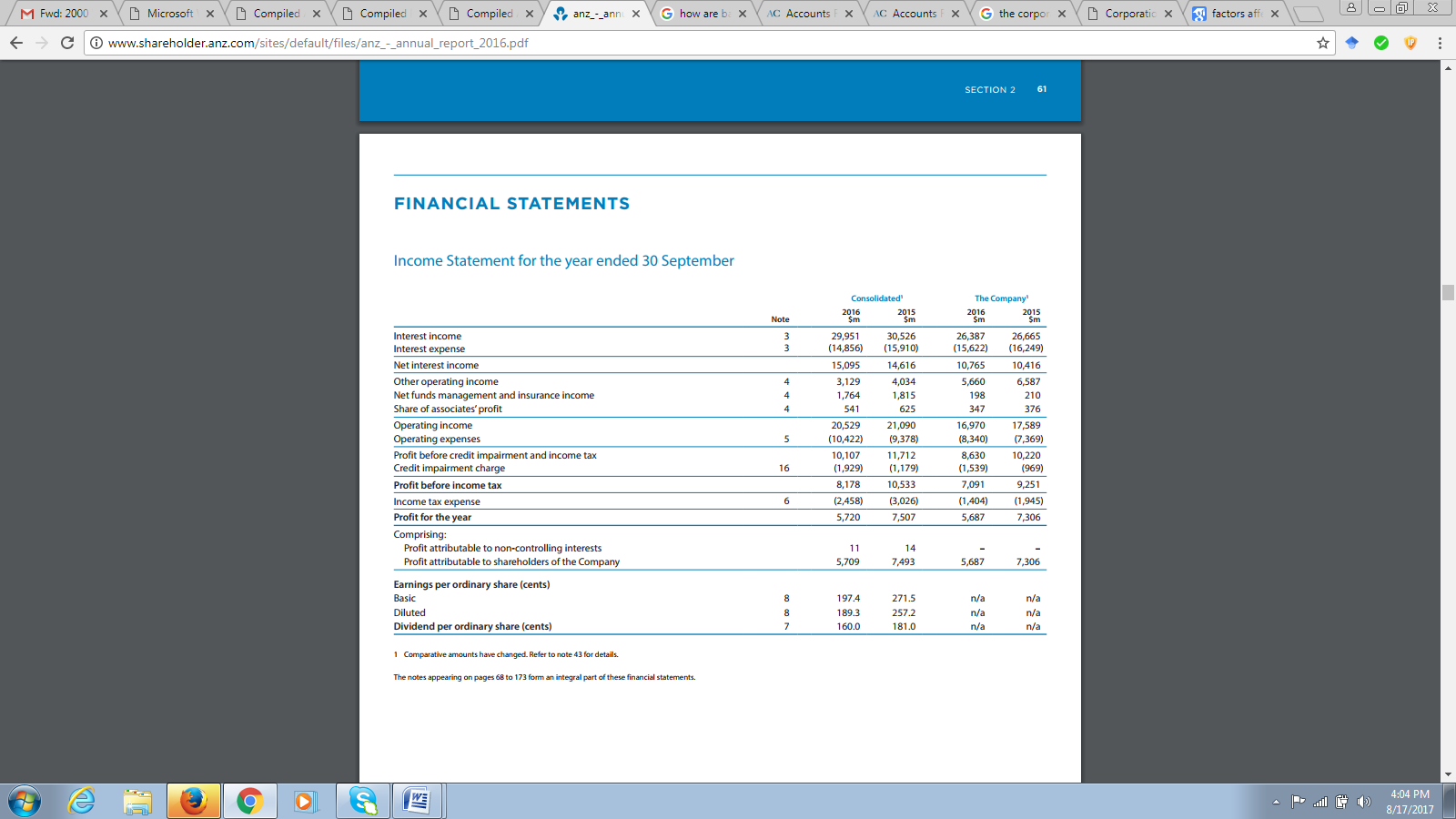

2016 Financial statement for ANZ , Income Statement

2016 Financial statement for ANZ , Balance Sheet

Delivering a high-quality product at a reasonable price is not enough anymore.

That’s why we have developed 5 beneficial guarantees that will make your experience with our service enjoyable, easy, and safe.

You have to be 100% sure of the quality of your product to give a money-back guarantee. This describes us perfectly. Make sure that this guarantee is totally transparent.

Read moreEach paper is composed from scratch, according to your instructions. It is then checked by our plagiarism-detection software. There is no gap where plagiarism could squeeze in.

Read moreThanks to our free revisions, there is no way for you to be unsatisfied. We will work on your paper until you are completely happy with the result.

Read moreYour email is safe, as we store it according to international data protection rules. Your bank details are secure, as we use only reliable payment systems.

Read moreBy sending us your money, you buy the service we provide. Check out our terms and conditions if you prefer business talks to be laid out in official language.

Read more